Investment Commentary April 2026

April 2026 Investment Commentary

Imagine that in January of 2020, someone told you that within a matter of months, the world would be hit by the worst global pandemic of our lifetime. Over 7 million confirmed deaths would follow. Much of the developed world would shut down economically. Businesses would close, travel would halt, and daily life as we knew it would be disrupted.

How many of you would have then predicted that the S&P 500 would end the year up 18.4%?(1) Yet that is exactly what happened. The lesson is that even when fear is justified, markets do not always respond in the way we expect.

That lesson is especially relevant today, because once again, there are plenty of legitimate reasons to worry. Consumer finances, particularly among the lowest-income Americans, are strained, with auto loan and credit card balances that are 90 or more days delinquent having hit their highest levels since 1999 and 2011, respectively.(2) Employment growth would now be negative were it not for the healthcare sector.(3) And the global economy is slowing down the longer the Strait of Hormuz stays closed due to the war in Iran, potentially putting nations that are dependent on oil imports (unlike the U.S., which became an oil exporter in 2019) into crisis. Europe alone still imports more than half of its energy needs, while Japan imports nearly all its fuel needs.(4)

Taken together, those concerns form a perfectly reasonable bearish narrative. However, one can also create optimistic narratives about the future. Roughly $335 billion in tax refunds are expected to be paid out in the first half of this year, up about 11.2% from last year, providing an influx of cash to American consumers.(5) Additionally, a recent poll of business owners shows that nearly one-third expect to increase their employee headcount over the next 12 months, and more than half anticipate wage increases of at least 5%.(6)

So which narrative is right? Probably neither in its entirety, and that is the point.

Our job as intelligent investors is not to aimlessly predict which narrative will be correct. Human beings tend to be far more confident in their forecasting ability than they should be, and that overconfidence often turns investing into speculation. By staying humble and accepting the flaws that come with human nature, we can make more disciplined decisions in the face of uncertainty.

In practice, that means focusing on two seemingly simple tenets:

1) Focus on Quality: Human nature will inevitably push the stock market to view companies with exuberant optimism or extreme pessimism at various points in time. However, by investing in quality companies with strong balance sheets and durable competitive advantages, you can increase the probability of building wealth over time.

2) Look at Probabilities, Not Predictions: By looking at the past and extrapolating how relevant it is in today’s environment, you can ground your investments in something beyond narratives. Two examples we are looking at currently are:

• Midterm Elections: At this point, the odds appear high that Democrats will win back the House. Relative to how they performed in 2024, they only need to gain three seats. Historically, the party not controlling the White House has gained at least three House seats in 18 of the last 20 midterm cycles since World War II. Market history around midterm elections is also instructive.(7) The average second and third-quarter stock market returns during midterm years have been -0.7% and +0.1%, respectively, compared with +6.7% in the fourth quarter (after election results are known).(8) This implies that the stock market will have increased volatility and muted returns leading up to November until investors can discern what the new power dynamics in Washington will mean.

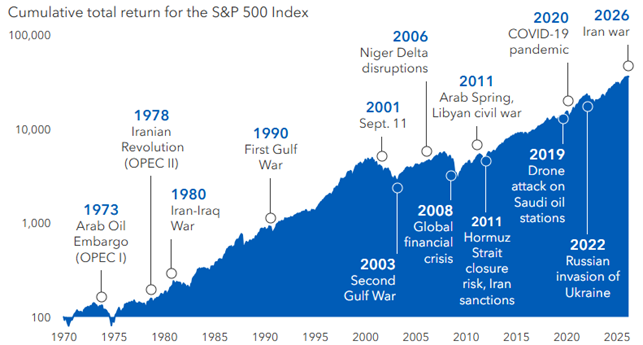

• War in Iran: Every new geopolitical conflict feels unprecedented while we are living through it, and each one seems capable of permanently derailing markets. Yet history has often told a more resilient story. The Dow rose 43% during World War I and 50% during World War II, while the S&P 500 posted double-digit gains in the 12 months following the Korean War, the Cuban Missile Crisis, the Gulf War, and the Iraq invasion.(9) None of this diminishes the human tragedy of conflict. One only has to look at the chart below to see that markets have historically adapted more quickly than investor emotions do.

There will always be reasons to fear. There will usually also be reasons to hope. The challenge is not eliminating uncertainty. The challenge is refusing to let uncertainty push us into emotional, short-sighted decisions.

Wishing you a wonderful spring season,

The Glen Eagle Investment Team

Disclosure: This commentary is furnished for the use of Glen Eagle Advisors, LLC, an SEC Registered Investment Advisor; Glen Eagle Wealth, LLC, Member FINRA & SIPC. The information presented is believed to be factual and up to date, but we do not guarantee its accuracy and is subject to change without notice. Commentary is for informational purposes only and is not meant to be investment advice or a recommendation of securities to any individual. It is not prepared with respect to the specific objectives, financial situation, or particular needs of any specific person. Investors reading this commentary should consult with their

Glen Eagle representative regarding the appropriateness of investing in any securities or adapting any investment strategies discussed in this commentary.

1. S&P Global “Driven by big tech's pandemic gains, S&P 500's 2020 surge masks uneven recovery” 2. First Trust "Stocks See Troubles Brewing" 3. WSJ - “ Why Healthcare Is Doing the Heavy Lifting in This Job Market 4. Barron’s – “What the Iran War Really Means for the Stock Market” 5. WSJ "Markets A.M.: Tax Refund Season Got a Bit Less Beautiful" 6. MFS – “Beyond the News" 7. First Trust “Election Year Forecast: A divided Congress” 8. BlackRock "Student of the Market April" 9. A Wealth of Common Sense – “Geopolitics vs. Markets

www.gleneagleadv.com