In our last Investment Commentary that we shared on April 6th, we encouraged our readers to maintain their composure despite the extreme market volatility that we were experiencing due to the impending tariffs of President Trump’s “Liberation Day”:

It is during these types of rapid market downfalls…that intelligent investors can distinguish themselves from the crowd - by maintaining control over their emotions…history has shown us that the one true way to permanently destroy wealth is by selling out of the majority of one’s stocks in the midst of a market correction. Over time, corporations have proved resilient and continued to innovate and increase their earnings, and, thus, their stock price.

We did not predict the speed at which the market would reward investors who kept their cool. Just two days after the stock market bottomed out, it then went on to reach an all-time high on June 27th, making it the fastest rebound from a 15%+ decline in history. (1)

However, this does not imply that investors will experience smooth sailing ahead. The stock market and economy are still actively digesting what the current reshuffling of the world order means for the future, and there are plenty of worrying data points. For example, since December 2024, China’s share of exports to the U.S. has declined from 15% to 9%, which is likely to increase the cost of some goods for American businesses and consumers. (2) Additionally, over the long term, the U.S. economy is likely to experience slower growth due to the government’s growing debt burden. As a nation, we currently pay $3.3 billion in interest payments every single day, and for every dollar the US government collects in tax revenue, about twenty cents goes to paying interest on debt rather than improving roads, schools, or healthcare. To put that in perspective, if we divided the national debt evenly across all U.S. households, each household would owe an astounding $273,914. (3

It would be a mistake, however, to view these types of challenges and the stock market’s return to a new all-time high as indications that another correction or downturn is imminent. In fact, since 1950, the average return for an investor who invested in the stock market at an all-time high was 9.4% and 29.1% over the next one-year and three-year periods, respectively. (4)

So, given all the above, what areas should investors be looking at in this environment, which is full of uncertainty?

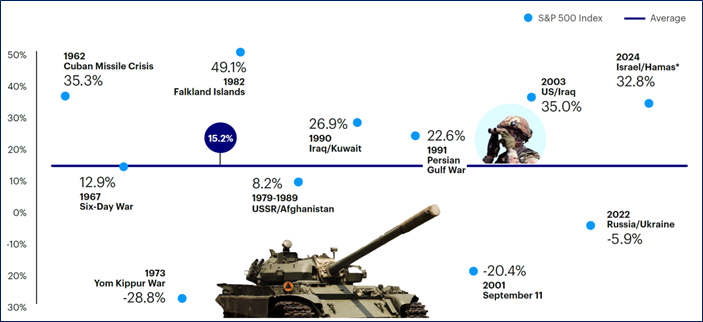

1) Defense Stocks: Ongoing conflicts in Ukraine and the Middle East have raised concerns about potential market disruptions. However, history shows that major geopolitical events involving military conflict since the 1960s have been followed by strong market performance, with the S&P 500 returning an average of 15.2% one year later. (7) These events also tend to boost demand for defense-related products and services. This is particularly true now with NATO members—Germany included—aiming to raise defense spending to as much as 5% of GDP. As globalization retreats and new spheres of influence form among global powers, we expect defense spending to remain a tailwind for select companies in the sector.

2) International Stocks: Since 1970, periods of U.S. dollar weakness have consistently led to international stocks outperforming U.S. stocks—and 2025 is no exception.(5) While the U.S. remains a global leader in innovation and entrepreneurship—having produced 241 companies worth over $10 billion over the last 50 years compared to just 14 in Europe—the rest of the world has been largely overlooked by investors. (6) Given how inexpensive international stocks are today and the potential for a continued dollar decline, adding some exposure could benefit most American investors, who are currently under-allocated. We are not suggesting an overweight position, but a modest allocation could improve long-term diversification.

3) Dividend Stocks: While we have previously shared our positive outlook on dividend-paying stocks, current market conditions and new academic research warrant renewed attention to these income-generating investments. Over the past 50 years, data from Ned Davis Research shows that S&P 500 dividend-paying stocks delivered an annualized return of 9.2%, compared to just 4.3% for non-dividend payers—with significantly lower volatility. (8) In today’s environment—where political headlines have driven sharp market swings in both directions—focusing on dividend stocks can help shift portfolios toward higher-quality companies while offering greater downside protection.

As an Investment Committee, we hope the three areas discussed above provide helpful context as we navigate the second half of the year. That said, now is also an ideal time to step back and reassess your overall portfolio—beyond specific geographies or sectors.

The market downturn we experienced in April revealed an important truth for many investors: there is often a gap between the desire for long-term growth and the ability to emotionally withstand short-term volatility. The recent rapid rebound offers a rare second chance for those who found the downturn unsettling. Now is the time to ensure your equity allocation truly reflects your risk tolerance—before the next period of market stress.

Wishing you a fun-filled rest of your summer with family and friends,

The Glen Eagle Investment Team

Disclosure: This commentary is furnished for the use of Glen Eagle Advisors, LLC, an SEC Registered Investment Advisor; Glen Eagle Wealth, LLC, Member FINRA & SIPC. The information presented is believed to be factual and up to date, but we do not guarantee its accuracy and is subject to change without notice. Commentary is for informational purposes only and is not meant to be investment advice or a recommendation of securities to any individual. It is not prepared with respect to the specific objectives, financial situation, or particular needs of any specific person. Investors reading this commentary should consult with their Glen Eagle representative regarding the appropriateness of investing in any securities or adapting any investment strategies discussed in this commentary.

Graphic above comes from Invesco “Military conflicts tend to not derail the market”. 1. Wall Street Journal - "Historic Rebound Sends S&P 500 to New Highs"2. Apollo – “China Selling Less to the US and More to Europe, Asia, and Latin America” 3. US Senate JEC’s Monthly Debt Update – July 2025 4. Ritholtz – “All Time Highs Are Bullish 06.26.25 5. Capital Group “Stock market outlook: Broader opportunities emerge” 6. Wall Street Journal – “The Tech Industry is Huge – and Europe’s Share of It Is Very Small” 7. Invesco – “Military Conflicts tend to not derail the markets”. 8. Wall Street Journal - “Dividends Aren’t Really About Cash”

Please feel free to share this newsletter with your network!